Calculate your tenant turnover rate easily with our free tool. Assess retention, spot trends, and improve property management today!

Understanding Tenant Retention with a Turnover Rate Calculator

Property management isn’t just about collecting rent—it’s about keeping your units occupied with happy tenants. One key metric to watch is how often renters move out, which directly impacts your bottom line through vacancy costs and re-leasing expenses. That’s where a tool to analyze tenant churn comes in handy. It gives property managers a clear snapshot of retention patterns without the headache of manual math.

Why Retention Metrics Matter

High move-out rates can signal deeper issues, like uncompetitive pricing or unresolved maintenance complaints. By calculating this percentage regularly, you can identify trends and act before small problems turn into empty units. Whether you manage a small apartment complex or a sprawling portfolio, having precise data helps you make informed decisions. Plus, comparing your stats against industry benchmarks (like the 40% threshold for concern) shows where you stand.

Take Control of Your Property’s Future

Don’t let guesswork guide your strategy. Using a simple analyzer for rental turnover equips you with the insights needed to improve tenant satisfaction and stabilize income. Plug in your numbers today and see the difference data can make in your day-to-day operations.

FAQs

What is a tenant turnover rate, and why does it matter?

It’s the percentage of tenants who move out over a specific period compared to your total units. Knowing this helps you gauge how well you’re retaining folks. High turnover often means unhappy tenants or issues with pricing, amenities, or management. Tracking it lets you spot problems early and make changes to keep your property thriving.

What’s considered a high turnover rate for rentals?

Generally, an annualized turnover rate above 40% is considered high in the property management world. If you’re seeing numbers like that, it might be time to dig into why tenants are leaving. Could be maintenance issues, rent hikes, or just a mismatch with the local market. Our tool flags this for you so you’re not left wondering.

How does the tool handle different time periods?

We’ve got you covered no matter how you track data. If you select a monthly or quarterly period, the tool automatically annualizes the rate by multiplying monthly figures by 12 or quarterly ones by 4. This way, you’re always comparing apples to apples, and you can benchmark against yearly industry standards easily.

Need to convert lease durations? Use our free Lease Term Converter to switch between days, weeks, months, and years in seconds!

.markdown

Understanding Lease Durations Made Easy

Navigating the terms of a rental agreement can sometimes feel like decoding a puzzle, especially when the duration is listed in a unit of time that doesn’t quite click for you. That’s where a tool like our Lease Term Converter comes in handy. Whether you’re a tenant trying to grasp how many weeks are left on a yearly contract or a landlord comparing rental periods, converting between days, weeks, months, and years shouldn’t be a chore.

Why Convert Lease Periods?

Rental agreements often vary in how they present timeframes—some might list a commitment in months, while others use years or even days for short-term stays. Having a quick way to translate these durations ensures you’re on the same page with everyone involved. Imagine planning a move and realizing your 18-month lease equates to roughly 78 weeks; that perspective might shift how you budget or schedule. Our tool simplifies this process, offering instant clarity without the need for manual calculations or guesswork.

A Tool for Everyone

From property managers to casual renters, understanding timeframes is key to smooth agreements. With just a few clicks, you can break down any rental duration into a format that makes sense to you. Try it out and take the confusion out of contracts!

FAQs

How does the Lease Term Converter calculate durations?

Our tool uses standard time conversions: 1 year equals 12 months, 52 weeks, or 365 days. When you input a duration and select a unit, it converts that value into all other units based on these ratios. We round the results to the nearest whole number to keep things clean and easy to read. So, if you enter 12 months, you’ll see it as 1 year, 52 weeks, and 365 days.

Can I use this tool for short-term or long-term leases?

Absolutely! Whether your lease is for a few days or spans several years, this converter handles it all. Just pop in the number and pick your unit, and it’ll show you the equivalent duration across all time units. It’s perfect for short-term rentals, yearly contracts, or anything in between. If you’ve got a tricky number, don’t worry—we’ll guide you if the input isn’t valid.

What if I enter a negative or invalid number?

No stress—we’ve got you covered. If you accidentally enter a negative number or leave the field blank, the tool will display a friendly error message asking you to input a valid, positive number. We keep it simple so you can quickly fix it and get your conversion results without any frustration.

Cloud property management software simplifies tasks like tenant communication, financial tracking, and maintenance management, all accessible from any device with an internet connection. By streamlining operations, these platforms save time, reduce errors, and support portfolio growth. Here’s what you should look for:

Tenant Management: Customizable online applications, advanced screening tools, automated lease tracking, and self-service portals for tenants.

Financial Tools: Automated rent collection, real-time profit and loss statements, expense tracking, and tax-ready reporting.

Maintenance Management: 24/7 request submission with attachments, automated work order management, and vendor tracking.

Marketing Features: Listing syndication, vacancy tracking, and performance analytics for filling units faster.

Document Management: Secure storage, e-signatures, and audit trails for easy access and compliance.

Reporting and Analytics: Customizable reports and portfolio-wide analytics to monitor performance.

Mobile Accessibility: Dedicated apps with real-time notifications, offline functionality, and remote access for on-the-go management.

These features not only simplify property management but also improve efficiency and tenant satisfaction. Whether you’re managing a few units or a large portfolio, the right software can make all the difference.

7 Must-Have Features in Cloud Property Management Software

Tenant Management Features

Managing tenants effectively starts with selecting the right individuals for your properties. A good cloud-based system should offer customizable online applications that gather essential details like Social Security numbers, employment history, and previous addresses, while also including a signed release of information. By digitizing this process, you eliminate the hassle of paper forms and ensure consistent data collection. From there, it’s all about thorough screening to maintain tenant quality.

Screening tools are a must-have. Look for platforms that provide key insights such as credit scores, payment history, debt-to-income ratios, and criminal background checks across various databases. Advanced tools can also search eviction records and verify identities to spot fraudulent income documents. For example, tools like ResidentScore are 15% better at predicting eviction risks compared to traditional credit scores. Additionally, modern income verification systems can confirm employment and income with an impressive 99.8% accuracy. Considering that tenant turnover costs average $3,872 per unit and eviction proceedings can surpass $5,000, the value of investing in robust screening tools becomes clear.

Tenant Screening

Built-in screening features should go beyond standard credit checks. A reliable system will pull data from specialized sources to verify Social Security numbers, check for financial risks like bankruptcies, and review eviction histories. Compliance matters too – choose software that includes Fair Credit Reporting Act (FCRA)-compliant forms and can generate automated "Adverse Action" notices for applicants who are denied.

A real-time dashboard is another essential feature, allowing you to track application statuses, screening progress, and approval decisions in one place. Some platforms even let you pass screening costs directly to applicants. Typically, this costs $17-$20 per report if you cover it or about $35 under applicant-pay models. It’s also wise to verify references from previous landlords rather than relying on current ones, as current landlords may give overly positive feedback to encourage a problematic tenant to move out.

Lease Tracking

Once tenants are screened, automated lease tracking can help you stay on top of lease terms. This feature ensures you never miss a renewal deadline by sending timely reminders to both you and your tenants. With only 63.8% of renters renewing their leases nationwide, proactive outreach can make a big difference in maintaining occupancy rates.

Automated lease templates that update with local and state law changes reduce legal risks. For instance, Connecticut limits security deposits to two months’ rent, while Georgia has no such limit. A robust tracking system should also integrate with your accounting tools, monitoring security deposits, pet deposits, and first/last month’s rent seamlessly. Real-time dashboards provide a clear view of lease statuses, balances owed, and upcoming vacancies across your portfolio.

Tenant Portals

Self-service portals simplify tenant interactions by offering 24/7 access to account details, lease documents, and maintenance requests. Tenants can submit maintenance requests with photos, make online payments, set up recurring rent payments, and upload important documents like insurance certificates.

These portals act as a communication hub, keeping all tenant interactions in one organized place. Push notifications can alert tenants about inspections, rent due dates, or maintenance updates. Mobile apps further enhance convenience, allowing tenants to manage everything from their phones. Property teams often save 60-80% of their time on compliance tasks with these integrated systems, and most platforms pay for themselves within 12-18 months through improved efficiency and reduced legal costs.

sbb-itb-9e51f47

Financial Tracking and Accounting

Effective financial tools can make property management much simpler. A good system should cover everything from automated rent collection to tax-ready reporting, giving you an up-to-date view of your portfolio’s financial health at any time.

Online Rent Collection

Automating rent collection eliminates the hassle of chasing payments and depositing checks. The best software sends automatic reminders before rent is due and notifies you of overdue payments. In fact, property managers report 90% fewer late payments when using features like automated reminders, late fees, and auto-pay options. The top platforms support various payment methods, including ACH bank transfers, credit cards, and debit cards. ACH transfers are often preferred because they have lower processing fees and settle within 1-2 business days.

Security is another key factor. Online platforms use data encryption and Two-Factor Authentication (2FA) to safeguard sensitive financial information, making them far more secure than paper checks, which display account numbers and signatures.

Once secure, automated rent collection is in place, tracking income becomes much easier. These systems also enable real-time financial reporting, keeping you informed at all times.

Profit and Loss Statements

Cloud-based software simplifies financial reporting by generating detailed income statements and rent rolls that break down revenue and expenses by property and unit. Real-time dashboards provide an instant overview of rent collected, outstanding balances, and the overall performance of your portfolio. With every transaction recorded at the unit level, payment statements and financial reports remain accurate and reliable. Additionally, locking financial records after filing ensures data integrity, which is crucial for audits.

Expense Tracking

Using spreadsheets for expense tracking can quickly become overwhelming as your portfolio grows. Automated tools solve this problem by categorizing and logging expenses – like maintenance costs and vendor invoices – without manual effort. Many systems integrate with a Chart of Accounts, streamlining tax preparation.

Automated bank reconciliation matches transactions with bank statements in real time, flagging discrepancies and reducing errors. The best platforms even convert maintenance work orders into bills and allow online vendor payments, ensuring all expenses are accurately recorded. Fixed costs, such as mortgages, insurance, and taxes, are also logged automatically, keeping financial records up-to-date.

Connecting your business bank accounts to the software creates a centralized view of all transactions, enabling you to identify trends and anomalies quickly. This integration also simplifies tax season by automatically preparing data for Schedule E tax forms and 1099s.

These financial tools work seamlessly with tenant and maintenance management features, offering a unified approach to property oversight.

Maintenance Management Features

Efficiently managing maintenance requests is critical for keeping tenants satisfied and maintaining property value. In fact, nearly 47% of renters consider maintenance the most important part of their living experience. The right tools can transform repair coordination into a smooth, trackable process, saving time and preventing costly emergencies. Here’s how key features in maintenance management software can make this happen.

Request Submission with Attachments

Tenant portals allow renters to submit maintenance requests 24/7, complete with photo or video attachments. These visuals help technicians diagnose issues faster and more accurately. Real-time updates – sent via email, push notifications, or SMS – keep tenants informed as their request moves through stages like "assigned", "in progress", and "completed." By automating maintenance tracking, property managers can save up to 20 hours a week compared to manually handling calls and spreadsheets. Once submitted, requests are seamlessly converted into actionable work orders, ensuring no task is overlooked.

Work Order Management

Good software automatically generates work orders and assigns them to the right technicians based on their skills, availability, and proximity. Centralized dashboards provide live updates on every open ticket, making it easy to track progress and avoid delays. Technicians can access unit histories and complete work orders directly from their smartphones, cutting 10 to 15 minutes per work order by eliminating paperwork. Automated reminders for overdue tasks or recurring maintenance – like HVAC filter changes – are essential, as emergency repairs can cost 3 to 5 times more than routine, planned maintenance.

Vendor Tracking

Keeping vendor details organized ensures reliable service and protects your business. Maintenance software should store vendor contacts, track insurance and licenses, and link invoices to accounting systems for an easy-to-follow audit trail. Performance tracking features let you evaluate metrics like completion times, response rates, and work quality. This data is invaluable for renegotiating contracts and deciding which vendors to keep. Real estate writer Tara Mastroeni highlights the importance of a strong vendor network:

A strong vendor network lets you handle maintenance requests faster and more affordably than scrambling for contractors each time.

Regularly auditing vendor performance can reduce overspending by 15%. This structured approach to managing maintenance ties seamlessly into other property management functions, creating a workflow that boosts efficiency across your portfolio.

Rental Listings and Marketing

If you’re looking to fill vacancies quickly, the internet is your best friend – 72% of renters start their search online. Cloud property software simplifies this process with tools like automated syndication and smart vacancy tracking.

Listing Syndication

Creating and managing rental listings manually can be a time sink. Instead, one-click syndication lets you distribute a master listing to major platforms like Zillow, Apartments.com, Realtor.com, and Zumper. For context, Zillow attracts over 200 million users, while Apartments.com sees more than 30 million monthly visitors each month. Jeremy Sine from CoSine Real Estate highlights the convenience:

"Buildium does a great job with vacancy listings. One click and it gets syndicated to dozens of different websites."

This automation can save you 2 to 4 hours per property. Plus, updates – whether it’s new photos, rent changes, or unit availability – sync across all platforms automatically. This ensures you avoid wasting time on inquiries about units that are no longer available. Some platforms even offer AI tools to generate polished property descriptions from your data.

Choosing the right platforms for your property type is key. Zillow tends to work best for single-family homes and condos, while Apartments.com is a better fit for larger multifamily buildings. Syndication expands your reach, but pairing it with vacancy tracking ensures you stay ahead of the game.

Vacancy Tracking

Vacancy tracking tools help you keep an eye on unit availability in real-time, so you can act before a unit sits empty. Visual timelines give you a clear view of current and upcoming occupancy, making it easier to spot gaps and launch automated marketing workflows.

Metrics like Time-to-Lease – the time it takes from listing a unit to signing a lease – can reveal whether your pricing, listing quality, or marketing channels need improvement. If this number exceeds your local market average, it might be time to tweak your approach. Another useful metric is the show-to-application rate, which can indicate if your listings align with renters’ expectations.

When a unit is marked as "occupied", most syndication tools automatically remove the listing from partner sites within 24 hours, eliminating dead leads. This seamless integration between vacancy tracking and listing management ensures your marketing stays focused on available units. Plus, performance reports analyze unit downtime and help identify which campaigns bring in the best leads.

Platforms like Renting Well combine these features, offering property managers an efficient way to syndicate listings and monitor vacancies in real time. This proactive approach not only streamlines your marketing efforts but also enhances overall property management.

Document Management and E-Signatures

Managing a property portfolio often comes with an overwhelming amount of paperwork. This is where centralized, cloud-based document storage steps in to simplify the process. By consolidating critical documents – like leases, applications, maintenance records, and tax files – into one secure location, property managers can save time and reduce inefficiencies. Without centralization, retrieving documents can turn into a time-consuming hassle. Cloud-based solutions solve this by making all files accessible from anywhere. In fact, in 2022, 78% of property managers sought software upgrades to improve document storage and retrieval. Better yet, centralizing data can cut document retrieval times by up to 70%.

Secure Document Storage

When handling sensitive information such as social security numbers, bank details, and signed leases, security is non-negotiable. The right software should include 256-bit encryption for both stored and transmitted data. Features like multi-factor authentication and role-based access controls ensure that users only access information relevant to their roles.

To avoid data loss, automatic backups across multiple locations are essential. Additionally, audit trails provide a detailed log of every action taken on a document, including who accessed it, when, and from which IP address. As Renting Well highlights:

All personal data in the application is encrypted and backed up regularly to ensure the absolute integrity of your property portfolio.

These tools not only enhance document control but also help property managers reduce legal risks by up to 60%.

Digital Lease Signing

Secure storage is just one part of the equation – digital signing takes document management to the next level by speeding up lease finalization. E-signatures eliminate the need for printing, scanning, mailing, or in-person meetings. Tenants can sign leases directly from their mobile devices, streamlining the process. Rental expert Brentnie Daggett from Rentec Direct points out:

Moving quickly through a lease signing process means a shorter vacancy timeframe and increased revenue for landlords and property managers.

E-signatures are legally binding under the federal ESIGN Act and come with tamper-proof audit trails. Look for software that includes a certificate of completion, detailing who signed, the timestamp, and the IP address. Jake Belding from Buildium explains:

A complete audit trail creates a tamper-proof record showing who signed, when they signed, and from what IP address, giving you a certificate of completion for your records.

The best platforms also include features like document routing and automatic reminders for pending signatures. Once the process is complete, signed documents are automatically saved in the tenant’s file library, ensuring everything stays organized and nothing gets misplaced.

Reporting and Analytics

Effective reporting and analytics transform raw data into actionable insights, enabling property managers to make informed decisions. Without the right tools, data can feel overwhelming and unhelpful. But with automated reporting, you can streamline monitoring and focus on the metrics that truly impact performance.

Customizable Reports

Financial reports should provide a clear, real-time snapshot of your portfolio. Tools like income statements and rent rolls show where you stand at any given moment, while detailed breakdowns allow you to filter revenue and expenses by property or unit. This level of specificity makes it easier to pinpoint which properties are thriving and which may need attention. As Renting Well explains:

Understanding your numbers gives you the knowledge and power to make important decisions.

In addition to standard financials, look for software that tracks investment metrics such as net income rate, cap rates, and rental yield. Operational reports – covering areas like vacancy rates, maintenance costs, and rent comparisons – help you stay ahead of market trends and plan for future expenses. Many platforms even format these reports to be print-ready, making it simple to share them with accountants or bookkeepers during audits or year-end reviews.

Experts recommend tracking at least seven essential reports monthly to stay on top of portfolio health. Tools for comparing rents and profits can refine your leasing strategies, while maintenance cost estimators help you avoid unexpected financial hits. These customizable reports lay the groundwork for deeper, portfolio-wide analysis.

Portfolio Analytics

Portfolio analytics consolidate all your financial data in one place, allowing you to monitor performance across multiple properties without juggling spreadsheets. Advanced tools powered by AI can identify trends and flag irregularities that might go unnoticed during manual reviews. In fact, landlords using property management software often save up to 20 hours per week compared to manual methods.

The best systems let you move seamlessly between a portfolio-wide view and granular, unit-level details. You can monitor metrics like occupancy rates, maintenance expenses, and tenant payment histories across your entire portfolio, then zoom in on specific properties that need closer attention. Filtering options also allow you to compare performance across ownership groups or property types, making it easier to identify underperforming assets.

Automation enhances these capabilities even further. For example, you can schedule income and expense reports or owner statements to be emailed automatically – say, on the 5th of each month – ensuring consistent oversight without manual effort. Nathan Miller, President of Rentec Direct, highlights the convenience of this feature:

One of the standout features of the new reporting functions is the option to automatically share reports via email with your owners and property managers. It’s a huge time saver.

Mobile Accessibility

Property management has gone mobile, and for good reason. With 60% of all web traffic now coming from mobile devices, managing properties on the go is no longer optional – it’s essential. Whether you’re juggling tenant meetings, overseeing repairs, or dealing with emergencies, mobile-friendly tools make it possible to handle your entire portfolio from anywhere.

Dedicated mobile apps for iOS and Android are game-changers. They offer smoother performance and access to key device features like cameras and GPS, which are crucial for tasks like on-site inspections and documenting maintenance issues. Some platforms even go a step further with offline functionality, allowing you to log data or file reports in areas without cell service. Once you’re back online, everything syncs automatically.

These mobile tools make it easier to tackle on-site tasks like inspections, maintenance, and even financial approvals. Plus, they enable real-time communication that keeps you connected and informed, no matter where you are.

Real-Time Notifications

Instant alerts are a lifesaver when you need to respond quickly. Push notifications for late payments, emergency maintenance requests, or new inquiries ensure you stay on top of urgent matters – even when you’re away from your desk. Instead of constantly refreshing your dashboard, these alerts bring critical updates straight to your phone.

The real power of these notifications lies in integration. When your communication tools are tied to your accounting and maintenance systems, you get the full picture before responding. Steven Salisbury from Rent Manager explains it well:

When communication lives inside the same system as accounting and maintenance data, property managers gain better context and can respond more efficiently, without jumping between platforms.

This setup lets you check payment histories while addressing maintenance issues or review financial trends before approving repairs – all from your phone. It’s not just about keeping property managers informed; automated alerts also keep tenants and owners in the loop with updates on maintenance schedules, policy changes, and rent reminders.

Paired with remote access features, these real-time notifications ensure you can act quickly and effectively, no matter where you are.

Remote Access

Remote access takes mobile management to the next level by letting you act on data instantly. For example, mobile platforms let you perform on-site inspections using customizable checklists, and you can attach photos or videos directly to reports. This eliminates the need to return to the office to document findings, speeding up the process of readying units for new tenants.

Financial management is just as seamless. Mobile-optimized portals allow property owners to access performance reports and financial statements 24/7. Meanwhile, you can approve expenses, process payments, or review profit and loss statements from the field. Tara Mastroeni, a real estate writer for Buildium, highlights how this benefits tenants:

For tenants, this technology will give them the ability to complete necessary tasks, such as paying rent, tracking the status of any maintenance requests, and communicating with you while on the go.

Conclusion

Selecting the right cloud-based property management software can redefine how your business operates. As Steven Salisbury from Rent Manager puts it:

Choosing property management software is a long-term decision that affects nearly every part of your operation, from accounting and leasing to reporting and resident communication.

The key is to align your specific challenges with features that solve them. Building a scorecard can simplify the decision-making process by focusing on critical needs like tenant management, financial tracking, maintenance workflows, and detailed reporting. This approach ensures the platform you choose meets your operational demands.

Security should also be a top priority. Look for platforms that implement AES-256 encryption, role-based access controls, and meet SOC 2 Type II compliance standards to safeguard your data and maintain smooth operations [10, 12].

Finally, take the software for a test drive. Renting Well provides a free trial with no credit card required, giving you the chance to explore its features firsthand [56, 60]. Compare its automation tools with your current manual processes to see how much time and effort you could save [60, 11].

FAQs

What security standards should cloud property software meet?

When it comes to cloud property software, robust security measures are non-negotiable. This includes implementing strong data encryption for both data in transit and at rest. Additionally, features like multifactor authentication, detailed access controls, and regular security audits are essential. The software should also adhere to industry standards such as PCI Level 1 and SOC 2 Type 2, ensuring the protection of sensitive tenant and financial information.

How do I choose features based on my portfolio size and property type?

When choosing features, consider the size of your portfolio and the type of properties you manage. Larger portfolios often require scalable tools, such as automated rent collection and lease management, to handle the workload efficiently. On the other hand, smaller portfolios may benefit more from software that prioritizes simplicity and ease of use.

For residential or multi-family properties, tenant management and maintenance tracking features are essential to streamline day-to-day operations. If you manage commercial properties, look for tools that offer robust financial reporting and secure document storage to meet your specific needs.

It’s also important to pick software that can adapt as your portfolio grows. Automation features are particularly helpful for improving efficiency and saving time as your business expands.

What should I test during a free trial before switching?

When exploring a free trial, focus on testing critical aspects like ease of use to ensure the software feels intuitive and straightforward. Look into mobile compatibility to confirm you can access it seamlessly across various devices. Dive into the core functionalities such as tenant management, rent collection, and financial reporting to ensure they align with your requirements.

Additionally, evaluate integration options to see how well the software connects with tools you already use. Consider its scalability to ensure it can handle portfolio growth, and don’t overlook customer support responsiveness – quick and helpful support can make a huge difference when challenges arise.

Compare rental prices across cities with our free Rent Comparison Tool. Find out if you’re overpaying for your studio, apartment, or house today!

Find the Best Rental Deals with a Rent Comparison Tool

Navigating the rental market can feel like a maze, especially when you’re trying to figure out if you’re getting a fair deal. That’s where a reliable rent comparison tool comes in handy. It’s a simple way to see how much you might pay for a studio, apartment, or house in different areas, helping you spot overpriced listings or hidden gems.

Why Compare Rental Prices?

Whether you’re a tenant planning a move or a landlord setting rates, understanding housing costs across locations is key. A tool that breaks down average rents between two cities or zip codes can save you hours of research. You’ll get a clear picture of market trends, like whether one area is significantly pricier than another, so you can budget smarter or price competitively.

Make Moving Decisions Easier

Relocating is stressful enough without worrying about rent surprises. By using a rental price comparison, you can weigh your options with confidence. Maybe you’ll discover a nearby city with lower costs for the same property type. Armed with this info, you’re better equipped to negotiate leases or choose the right spot to call home.

FAQs

How accurate are the rent prices in this tool?

Our Rent Comparison Tool uses simulated data to provide average rental prices based on typical market trends for different property types and locations. While it’s not tied to a live database, it offers a realistic starting point for comparisons. For the most current data, we recommend cross-checking with local listings or real estate platforms.

Can I compare rent for multiple property types at once?

Right now, the tool focuses on comparing a single property type at a time to keep the results clear and easy to digest. If you want to check multiple types, just run the tool again with a different selection. It’s quick and straightforward!

Who can benefit from using this rent comparison tool?

This tool is perfect for anyone in the rental game—tenants looking to move, landlords setting fair prices, or even real estate enthusiasts curious about market differences. Whether you’re budgeting for a new place or analyzing trends across cities, this tool helps you make informed decisions without the hassle.

Estimate your annual property maintenance costs with our free tool. Input property type, age, size, and location for an accurate breakdown!

Plan Smarter with a Property Maintenance Cost Estimator

Owning a property is a rewarding investment, but the upkeep can sneak up on you if you’re not prepared. Whether you’ve got a cozy single-family home, a bustling commercial space, or a rental apartment, annual maintenance expenses are a reality. That’s where a reliable tool to estimate property care costs comes in handy. It takes the guesswork out of budgeting by factoring in key details like the size of your space, how old it is, and whether you’re in a pricey urban area or a quieter rural spot.

Why Estimating Upkeep Costs Matters

Maintenance isn’t just about fixing a leaky faucet here or there—it’s about preserving the value of your asset over time. Without a clear idea of what you might spend each year, unexpected repairs can throw your finances off track. By using a calculator tailored to real estate maintenance budgets, you can plan for routine tasks like HVAC servicing or roof inspections before they turn into emergencies. Plus, understanding these costs helps if you’re buying, selling, or managing properties. Take a moment to input your details and get a personalized breakdown—it’s a small step that can save you big headaches down the road.

FAQs

How accurate is this property maintenance cost estimator?

Our tool provides a solid starting point based on industry-standard base costs per square foot, adjusted for age and location. For instance, older properties often need more repairs, so we bump up the cost by 10% per decade. Location matters too—urban areas tend to have higher labor rates, so we add 20% there. While it’s not a replacement for a professional quote, it’s a great way to get a ballpark figure for budgeting.

Can I use this tool for any type of property?

Absolutely! We’ve built this estimator to handle a range of property types, from single-family homes to apartments and even commercial spaces. Each type has a different base cost per square foot—$1.50 for homes, $1.20 for apartments, and $2.00 for commercial—to reflect varying maintenance needs. Just pick the one that fits, and we’ll tailor the estimate for you.

What if I enter incorrect or unrealistic data?

No worries—we’ve got you covered. If something looks off, like a negative age or an impossible size, the tool will prompt you to double-check your inputs. We want to make sure the estimate you get is as reliable as possible, so we’ll guide you to enter valid info before crunching the numbers.

Calculate rental yield instantly with our free tool! Evaluate property profitability by entering purchase price, rent, and expenses.

Maximize Your Property Returns with a Rental Yield Calculator

Investing in real estate can be incredibly rewarding, but only if you’ve got the right data to back your decisions. That’s where a tool to assess rental profitability comes in handy. It takes the guesswork out of evaluating potential investments by giving you a clear percentage that reflects your annual return based on rent and costs.

Why Calculating Property Returns Matters

Understanding the financial performance of a rental property is crucial before signing on the dotted line. By factoring in the purchase price, monthly income from tenants, and yearly expenses like taxes or repairs, you get a snapshot of whether the investment makes sense. This kind of insight helps you compare different properties or even decide if real estate is the right move compared to other opportunities.

Beyond the Numbers

While a solid percentage is a great starting point, don’t forget the bigger picture. Market conditions, property location, and future appreciation all play a role. Use this analysis as your foundation, then dig deeper into local trends to ensure you’re making a smart, informed choice. With the right approach, you’ll build a portfolio that delivers steady returns for years to come.

FAQs

What is rental yield, and why does it matter?

Rental yield is a measure of how much profit a property generates from rent, expressed as a percentage of its purchase price. It’s a key metric for investors because it shows whether a property will provide a good return compared to other investments. A higher yield often means a better cash flow, but you’ll also want to consider location, market trends, and long-term growth potential when making decisions.

What’s considered a good rental yield for a property?

A ‘good’ rental yield depends on your market and goals, but generally, anything above 5-6% is considered decent for most areas. In high-demand urban markets, yields might be lower due to higher property prices, while rural or up-and-coming areas could offer 8-10% or more. Always compare your yield to local averages and factor in risks like vacancy rates or unexpected repairs.

Can I use this tool for commercial properties too?

Absolutely, this calculator works for any type of rental property—residential or commercial. Just make sure you’ve got accurate figures for purchase price, monthly rent, and annual expenses. The formula stays the same, so you’ll get a clear picture of the yield regardless of property type. If you’ve got unique costs for commercial spaces, like longer vacancies, keep those in mind when interpreting the results.

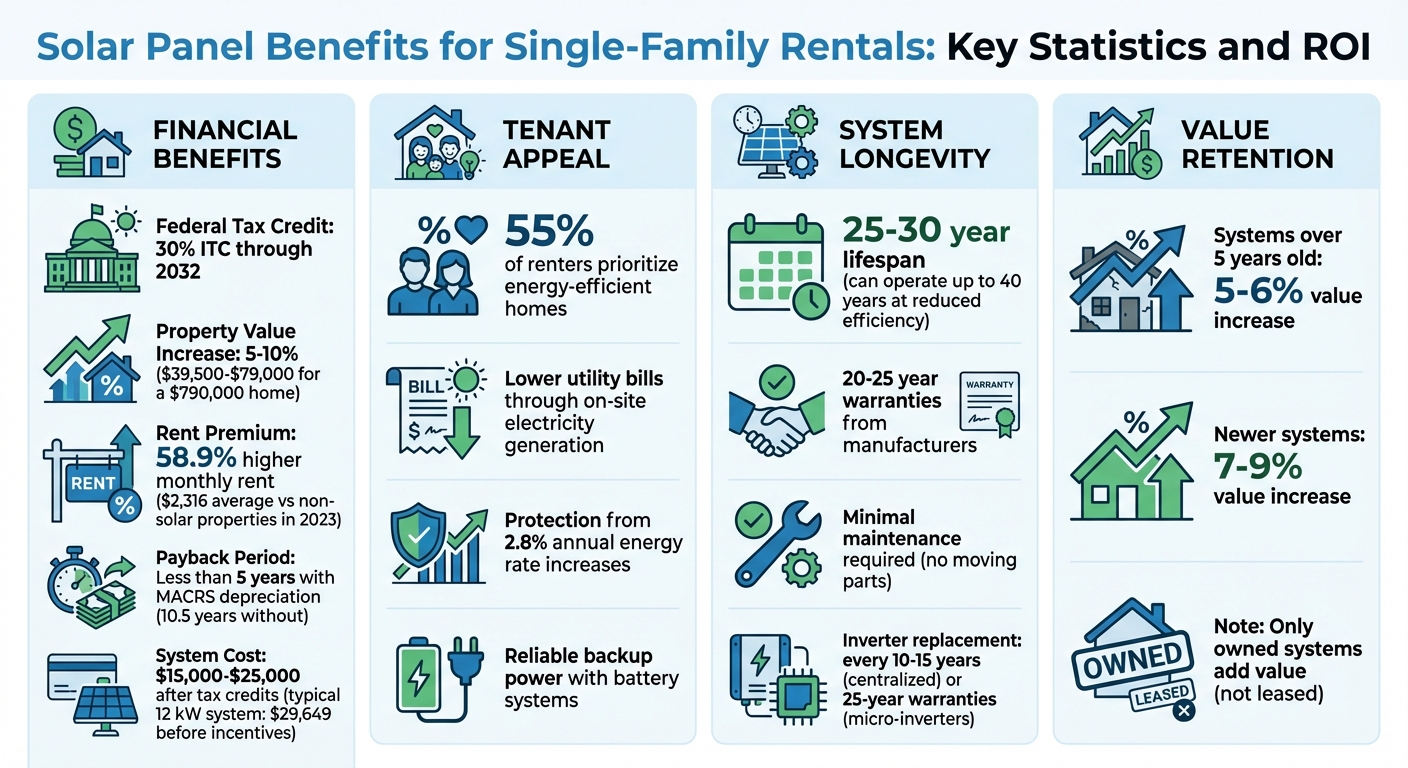

Solar panels reduce energy costs, increase rent potential and property value for single-family rentals, with tax credits, fast payback and low maintenance.

Solar panels are becoming a smart choice for single-family rental property owners. They help reduce energy costs, attract eco-conscious tenants, and increase property value. Here’s why they make sense:

Lower Costs: Solar panels cut electricity bills for landlords and tenants. Federal incentives, like the 30% tax credit, make installation more affordable.

Higher Rent Potential: Rentals with solar systems earned nearly 59% more in monthly rent in 2023 compared to those without.

Increased Property Value: Solar panels can add $15,000 or more to a home’s resale value.

Tenant Appeal: Over half of renters prioritize energy-efficient homes, and solar panels lower utility bills while offering reliable backup power with battery systems.

Affordable Installations: Costs for residential solar systems have dropped significantly, with prices now ranging from $15,000 to $25,000 after tax credits.

Solar panels are a win-win for landlords and tenants, offering financial savings, higher property value, and an edge in competitive rental markets.

Solar Panel Benefits for Single-Family Rentals: Key Statistics and ROI

Main Benefits of Solar Panels for Single-Family Rentals

Lower Operating Costs and Improved Cash Flow

For landlords who include utilities in the rent, solar panels can slash electricity costs right away. By generating your own power and selling any extra back to the grid through net metering, you can see a direct boost in your monthly cash flow.

Federal programs like the 30% Investment Tax Credit (ITC) and the Modified Accelerated Cost Recovery System (MACRS) make the initial investment much more manageable. MACRS allows you to depreciate the cost of solar equipment over five years, offering valuable tax deductions along the way.

Attracting Tenants and Supporting Higher Rents

Solar panels do more than just cut costs – they make your property more attractive to potential tenants. They help justify higher rents by reducing utility expenses and appeal to eco-conscious renters, which can lower turnover rates. And the numbers back this up: single-family rentals with solar energy commanded an average monthly rent of $2,316 in 2023 – 58.9% higher than non-solar properties.

"A solar-powered building is also a great marketing tool when it comes to renting out your unit: solar appeals to a growing segment of residents who care about the environment, and installing a solar energy system can help you attract tenants." – EnergySage

Adding battery storage to a solar system offers even more value. It provides backup power during outages, giving tenants a level of reliability and comfort that traditional rentals just can’t match.

Boosting Property Value

Solar panels don’t just save money – they also increase the overall value of your property. Among home improvements, solar installations deliver some of the best returns. In fact, they can often pay for themselves by driving up property value. For a home priced at $790,000, solar can add between $39,500 and $79,000 to its resale value.

Ownership is key here. Homes with owned solar systems typically see value increases of 5% to 10%, while leased or third-party-owned systems often add no value and may even complicate a sale. Even older systems hold their worth – installations over five years old can still add 5% to 6% in value, while newer systems see increases of 7% to 9%. This makes solar panels not just an energy solution but a smart long-term investment that enhances the overall marketability and worth of your property.

Addressing Common Concerns: Cost, Maintenance, and Risks

Installation Costs and Available Incentives

When installing solar panels, the upfront expenses typically include the cost of hardware, professional installation, grid connection fees, local permits, and sales tax. However, the Investment Tax Credit (ITC) offers a 30% offset on system costs for installations completed through 2032, with gradual reductions in the years that follow.

Landlords can also take advantage of a 10% annual depreciation benefit and may qualify for additional state rebates, utility programs, or Renewable Energy Certificates (RECs). For those looking to minimize upfront costs, solar leases or Power Purchase Agreements (PPAs) provide an option to install panels with little to no money down, though the tax credits remain with the third-party owner.

To ensure you’re making the best investment, get at least three bids from NABCEP-certified installers and confirm whether your utility company offers net metering. Beyond the initial costs, minimal maintenance and strategic planning can further enhance the value of your solar system.

Maintenance Requirements and Panel Lifespan

Solar panels are known for their low-maintenance requirements, which pair well with the financial benefits they offer. With no moving parts, they demand very little upkeep. Most panels have a lifespan of 25 to 30 years, and even after that, they can continue generating electricity – albeit at a reduced efficiency – for up to 40 years. Typically, manufacturers provide warranties ranging from 20 to 25 years.

While the panels themselves are durable, other components like centralized string inverters may need replacement every 10 to 15 years. Micro-inverters, on the other hand, often come with warranties that can last up to 25 years. Routine maintenance, such as periodic cleaning and inspections, generally incurs minimal costs. If you opt for a solar lease, ensure the agreement clearly outlines who is responsible for maintenance to avoid any misunderstandings later.

Evaluating Roof Condition and Installation Timing

Before installing solar panels, it’s crucial to assess the condition of your roof. A structurally sound roof not only minimizes risks but also ensures you can maximize the long-term benefits of your solar system. If your roof is nearing the end of its lifespan – say, within the next five to ten years – consider replacing it first to avoid the added expense of removing and reinstalling panels down the line. Additionally, verify that your roof can handle the weight of the system and accommodate any necessary repairs.

For optimal energy production in the U.S., south-facing roofs are ideal. Be sure to evaluate potential shading from nearby trees or buildings, factoring in future growth or construction that could impact sunlight exposure. It’s also important to review HOA guidelines or local building codes, as many states have "solar rights provisions" that limit restrictions on solar installations. Tools like Google Project Sunroof or the NREL PVWatts calculator can help you estimate your property’s solar potential using satellite imagery and weather data. By carefully timing your installation and ensuring your roof is ready, you can reduce risks and protect the added property value that solar panels can bring.

Should You Install Solar Panels on Your Rental Property?

sbb-itb-9e51f47

How Solar Panels Benefit Tenants

Solar panels don’t just boost landlords’ property value and cash flow – they also bring meaningful advantages to tenants, from slashing utility bills to offering peace of mind during power outages.

Lower Utility Bills and Predictable Energy Costs

Solar panels produce electricity right on-site, reducing the need to buy as much power from utility companies. With net metering, any excess energy generated during the day flows back to the grid, offsetting costs for nighttime or cloudy-day energy use.

Tenants can save even more by timing energy-heavy activities, like running the dishwasher or doing laundry, during peak sunlight hours when solar output is strongest. Adding a battery storage system takes these benefits further by storing surplus energy generated during the day for use at night, cutting reliance on the grid even more. Plus, solar systems often come with fixed electricity rates, shielding tenants from rising utility costs and making monthly budgeting easier. These savings not only reduce financial stress but also make solar-equipped properties more attractive to renters looking for eco-friendly and cost-effective living options.

Attracting Environmentally Conscious Renters

For Millennials and Gen Z renters, sustainability is a top priority. Research shows that 55% of renters actively look for eco-friendly features in their homes. Solar panels act as a visible indicator of a forward-thinking, energy-efficient property, helping it stand out in a crowded rental market.

"Tenants who benefit from lower energy expenses are more likely to stay." – Triumph Property Management

Solar-equipped properties align perfectly with the values of environmentally aware renters, who often seek to minimize their carbon footprint. This alignment not only attracts tenants but also leads to higher retention rates and fewer vacancies for landlords. Highlighting benefits like reduced bills and sustainability in rental listings can draw in tenants willing to pay more for a greener lifestyle.

Reliable Backup Power During Outages

Solar panels can also enhance reliability for tenants, especially when paired with battery storage systems. While solar panels alone don’t work during blackouts, a battery system can keep essential appliances running when the grid goes down. This feature is particularly valuable in areas with frequent outages or extreme weather, offering tenants a sense of security and convenience.

Battery systems can be customized to provide backup power for critical appliances or even the entire home. Landlords can use property tours to explain how these systems work, building trust and justifying higher rents. For tenants in regions prone to power disruptions, this added reliability becomes a standout amenity, improving satisfaction and increasing the likelihood of lease renewals.

Steps for Installing Solar Panels for Single-Family Rentals

Evaluating Feasibility and Return on Investment

Start by conducting an energy audit and reviewing the last 12 months of utility bills to determine your annual energy consumption in kilowatt-hours (kWh). This step ensures you can properly size your solar system, avoiding unnecessary costs from overestimating your energy needs.

Next, confirm that your roof meets the criteria for optimal solar performance, such as adequate sunlight exposure and structural integrity. You can use online tools to estimate your property’s solar potential.

For context, a typical 12 kW solar system costs around $29,649 before incentives. The 30% federal tax credit can significantly reduce this expense. If you purchase the system outright, you can expect to break even in about 10.5 years. For rental properties, using MACRS depreciation can lower the payback period to less than five years. To ensure you get the best deal, obtain quotes from at least three NABCEP-certified installers. Compare their cost-per-watt rates and projected annual energy production. Also, check whether your local utility offers net metering, which allows you to earn credits for any surplus energy your system generates and sends back to the grid.

These steps are essential for laying the groundwork to maximize the financial benefits of your solar investment.

Structuring Lease Terms for Solar-Equipped Properties

How you structure your lease will depend on who pays the electric bill. If you keep the electric bill in your name, the solar system can reduce your operating expenses. This allows you to offer a higher, flat-rate rent that includes electricity. On the other hand, if tenants are responsible for their own utility bills, you can justify a rent premium by emphasizing the savings they’ll see on their energy costs.

"To account for the upfront costs of installing solar, landlords and owners can charge additional rent and advertise that utilities are included." – Kaycee Miller, Rentec Direct

Make sure your lease specifies who is responsible for paying for electricity, how net metering credits will be handled, and whether tenants have any responsibilities related to monitoring the solar system. If you choose a solar lease or a power purchase agreement (PPA), remember that a third party owns the system. In this case, either you or your tenant will need to cover a fixed monthly fee or pay for the electricity generated at a discounted rate.

Using Property Management Software for Solar Tracking

After installing your solar system, it’s important to track its performance to maximize its benefits. Many solar providers offer proprietary software that monitors energy production and system health in real time. Additionally, property management platforms like Renting Well can serve as a central location for organizing important documents like installation records, interconnection permits, and warranties.

Use your property management software to track warranties, tax credits, Renewable Energy Certificates (RECs), and net metering savings. This makes reporting and monitoring your return on investment much easier. You can also set reminders for regular inspections or professional cleanings, ensuring your system continues to operate at peak efficiency.

Conclusion: Solar Panels Benefit Landlords and Tenants

Solar panels offer landlords a chance to see strong financial returns, thanks to incentives like the 30% federal tax credit and MACRS depreciation. These benefits can reduce payback periods to less than five years. Additionally, solar installations increase property values by 4%–10%, which translates to an added $39,500 to $79,000 on a home valued at $790,000 – far surpassing the typical 50–60% return on investment seen with kitchen or bathroom upgrades.

For tenants, the advantages are clear: lower monthly utility bills and insulation from the historical 2.8% annual rise in energy rates. This creates a mutually beneficial arrangement – landlords can justify higher rents while tenants enjoy real savings. Plus, properties with solar panels attract the growing number of renters (55%) who prioritize eco-friendly features when selecting a home.

"Solar panels are viewed as upgrades, just like a renovated kitchen or a finished basement." – Lawrence Berkeley National Laboratory

Concerns about costs and maintenance are manageable. Solar systems come with warranties lasting 20–25 years, ensuring decades of affordable energy after the initial investment. By evaluating feasibility and setting clear lease terms, landlords can maximize their financial gains.

Tools like Renting Well make it easier to track warranties, tax credits, and system performance, simplifying the process of monitoring returns. With equipment costs at historic lows and incentives locked in through 2032, now is an excellent time to consider solar for single-family rentals.

FAQs

Can installing solar panels increase the rent for single-family rentals?

Adding solar panels can often support a slight rent increase. Many tenants are open to paying a bit more for homes that offer lower electricity bills and eco-friendly benefits. In some markets, this might translate to an additional couple of hundred dollars each month. Solar panels not only appeal to renters who value sustainability but also enhance the long-term worth of your property.

What kind of maintenance do solar panels need on rental properties?

Solar panels are a hassle-free addition to rental properties, requiring only a bit of routine care to keep them in top shape. For landlords, the main upkeep involves occasional cleaning to clear away dirt and debris, trimming back trees or shrubs to prevent shading, and visual inspections to spot any signs of damage or wear.

While the panels themselves are built to last, inverters typically need replacing every 5–10 years. Adding critter guards is another smart move to protect the system from pests. Most solar panels come with warranties that cover repairs for manufacturing defects or performance concerns, which can offer some extra reassurance. Keeping an eye on energy output regularly is also a good way to confirm the system is running smoothly.

Do solar panels boost the resale value of rental properties?

Yes, installing solar panels can boost the resale value of a rental property. Research shows that solar installations can add about $5,900 per kilowatt (kW) of installed capacity to a home’s value. In some cases, properties equipped with solar panels have experienced value increases as high as $79,000.

For landlords, this means solar panels aren’t just an eco-friendly upgrade – they’re a strategic investment. They enhance a property’s appeal and can improve profitability over time, particularly in areas where energy efficiency is highly valued.

Discover expert tips on identifying rental scams, understanding leasing challenges, and improving tenant screening processes.

In the increasingly complex world of property management, leasing isn’t just about filling vacancies anymore – it’s a nuanced blend of art, science, and strategy. The rental market has evolved significantly over the past few years, bringing both opportunities and challenges for property owners and managers. From combating rental fraud to staying competitive in markets saturated with new inventory, effective leasing is more critical than ever.

This guide explores key insights shared by Brett Dreau, a seasoned leasing expert, during a detailed discussion about modern leasing challenges and strategies. Whether you own one property or manage hundreds, understanding the dynamics of leasing can significantly impact your profitability and peace of mind.

The Shifting Landscape of Leasing: More Than Just a Sign in the Yard

Gone are the days when leasing meant sticking a "For Rent" sign in the yard, putting up a listing, and watching tenants flock to you. According to Brett, leasing has become increasingly competitive and technology-driven, with renters now evaluating landlords and property managers as rigorously as they are being evaluated themselves.

Challenges in Leasing Today

Increased Supply: Many markets, particularly in the Sunbelt and Mid-Atlantic regions, are seeing an influx of new build-to-rent properties. These homes are often larger, more modern, and come with enticing concessions, such as one or two months of free rent. For older properties, competing with this new inventory can be tough.

Evolving Renter Expectations: Renters today demand more than just a roof over their heads. They’re looking for responsive management, secure neighborhoods, and sometimes even smart home technology. A poor leasing experience or delayed communication can lead to skepticism about how a landlord might handle maintenance or other issues.

Economic Pressures: With renters more rent-burdened than ever, price becomes a critical sticking point. While concessions can help, they often eat into property owners’ margins.

Rental Fraud: Alarmingly, fraud has become a significant issue, with 7–12% of applications in some markets being outright fraudulent. This includes fake IDs, falsified income documents, and other deceptive practices that make thorough screening essential.

The Role of Technology in Modern Leasing

Technology plays a pivotal role in navigating these challenges. Platforms like ID verification tools, applications that flag fraudulent submissions, and leasing CRMs have become integral to protecting properties and ensuring smooth leasing operations. However, as Brett emphasizes, technology should enhance human judgment, not replace it.

sbb-itb-9e51f47

Key Strategies to Master Leasing in 2025

To succeed in today’s leasing landscape, property owners and managers must adopt a strategic and empathetic approach. These strategies can help:

1. Win Tenant Trust Quickly

Renters are evaluating you as much as you’re vetting them. From the first interaction, demonstrate responsiveness and professionalism. Picking up the phone promptly and addressing concerns with empathy can set the right tone.

A common renter concern is property management responsiveness. Slow application processes or poor communication during leasing can create doubt about how maintenance or disputes might be handled later.

2. Master the Art of Overcoming Objections

Price, neighborhood safety, and property features are often sticking points for renters. Leasing teams must be equipped to address these concerns effectively, whether it’s by explaining the value of the home, highlighting community benefits, or offering concessions.

Understanding the local market is critical. For example, if a home is in a gentrifying neighborhood or next to boarded-up properties, having honest yet optimistic conversations about the area can help renters see potential.

3. Leverage Data and Pricing Expertise

Pricing a rental property correctly is both an art and a science. Tools that rely on algorithms, like Zillow’s Zestimate, often miss key nuances such as home type, square footage, and unique property features. A 4,000-square-foot home sounds appealing but could be overwhelming for potential tenants worried about furnishing or cleaning such a large space.

Utilize detailed market research to guide pricing decisions. Consider lead volume and local demand trends. For example, Brett highlighted a market in Alabama where properties averaged only three leads per month. In such cases, drastic measures like rent reductions or offering concessions might be necessary to avoid prolonged vacancies.

4. Adopt a Proactive Fraud Prevention Strategy

Fraudulent rental applications are a growing concern, especially in high-risk markets like Atlanta and Memphis. Property managers must use advanced screening tools, such as ID verification and income checks, to spot fraud before it creates problems.

Even with technology, staying vigilant is crucial. Train leasing teams to recognize red flags like inconsistent documents or unverifiable references.

5. Enhance the Resident Experience

Property managers should focus on creating a seamless move-in experience. Introducing roles like move-in coordinators, who guide renters through initial steps, can ensure tenants feel supported and informed.

Additionally, maintaining clear communication about responsibilities, payments, and property features can prevent misunderstandings later.

6. Prepare for Market Cycles

Demand fluctuates seasonally, with peak leasing periods typically running from early spring to late summer. Owners should aim to list properties before markets slow down in mid-November.

As Brett noted, recent years have seen more pronounced slow seasons, requiring property managers to be even more strategic during low-demand months.

The Future of Leasing Technology: What’s Next?

While technology has revolutionized leasing, there’s still room for growth. Potential developments include:

Better Smart Home Integration: Renters are increasingly drawn to properties with smart home features like thermostats, automated sprinklers, and security systems. However, challenges like device reliability and battery life must be addressed before widespread adoption becomes practical.

Enhanced Fraud Detection: As fraudsters grow more sophisticated, so must screening tools. Future systems may leverage AI to analyze application patterns or flag suspicious activity.

Reduced Friction in Access Control: Tools like Bluetooth-enabled lockboxes and digital keys make showings more efficient but can create barriers for legitimate renters. Finding the right balance between security and convenience will be key.

Key Takeaways

Leasing is both art and science – technology and human judgment must work together to provide an excellent tenant experience.

Rental fraud is a significant risk, with 7–12% of applications in some markets being fraudulent. Advanced screening tools are essential.

Pricing requires deep market knowledge, as automated tools often overlook important details like home type and unique features.

Empathy and responsiveness build trust with tenants, setting the stage for a positive landlord-tenant relationship.

Neighborhood perception matters – leasing teams should be prepared to address renter concerns about safety and amenities.

Smart home features are increasingly desirable, but technological reliability remains a hurdle.

Seasonal trends affect demand, so owners should strategize listings around peak leasing months to avoid prolonged vacancies.

Conclusion

For property managers and owners, successful leasing means more than just finding a tenant – it’s about finding the right tenant while protecting the property and maximizing profitability. By combining technology, rigorous screening processes, and an empathetic approach to renter concerns, landlords can navigate even the most challenging markets.

As Brett Dreau aptly put it, leasing is not just a transactional process but a strategic endeavor that requires both data-driven decisions and human insight. With the right tools and mindset, landlords can not only survive but thrive in today’s rental housing market.

Discover practical tips for effective rental property management, including tenant screening, legal docs, and boosting cash flow.

Managing rental properties effectively is both an art and a science. For property owners, landlords, and managers, balancing tenant satisfaction, compliance with legalities, and the drive for profitability can feel overwhelming. However, with the right strategies, systems, and mindset, rental property management can become a streamlined process that enhances both income and long-term asset value.

Drawing on insights from experienced property managers and investors with years of hands-on experience, this article explores the critical components of successful property management. Whether you’re self-managing or considering hiring professionals, this comprehensive guide will help you build better tenant relationships, protect your investments, and maximize returns. And if you’re looking for a real estate investor service provider, then you may consider checking out https://nerdbot.com/2025/10/28/how-to-find-a-real-estate-investor-service-provider/ for more info.

Why Property Management Matters

Effective property management is the backbone of rental property success. At its core, property management is about ensuring that your real estate investments generate steady cash flow and grow in value over time. Poor management, on the other hand, can lead to vacancies, high tenant turnover, legal troubles, and even asset devaluation.

Here’s why good property management is essential:

Increased Cash Flow: By minimizing vacancies, reducing maintenance costs, and fostering tenant satisfaction, you can maximize rental income.

Asset Protection: Well-maintained properties retain value and attract better tenants.

Wealth Building: Smart management enhances your net worth through debt reduction, property appreciation, and consistent cash flow.

Liability Mitigation: Avoid legal trouble by adhering to landlord-tenant laws and fair housing regulations.

Whether you manage properties yourself or hire professionals, the ultimate goal is the same: create a smooth-running operation that protects your investment and generates predictable results.

sbb-itb-9e51f47

Key Components of Successful Property Management

1. Tenant Screening: Choosing the Right Tenants

Tenant screening is one of the most critical steps in property management. A well-qualified tenant minimizes the risks of unpaid rent, property damage, and constant turnover. Here’s how to build a robust tenant screening process:

Require Comprehensive Applications: Every potential tenant should submit a detailed application with accurate rental and employment history.

Verify Information: Confirm credit scores, rental history (check for evictions), and employment details. A good rule of thumb is requiring income to be at least three times the monthly rent.

Set Clear Standards: Establish minimum credit requirements and stick to them. Consistency protects you from violating Fair Housing laws.

Collect Application Fees: A small fee demonstrates tenant seriousness and covers the cost of background checks.

Beware of Scams: Some tenants may fabricate documents, especially on unverified platforms like Zillow. Always cross-check information and documentation.

2. Legal Compliance and Documentation

Property management involves a significant amount of paperwork. Properly drafted and maintained legal documents protect you from disputes.

Leases: Use legally vetted leases tailored to local laws. Avoid generic templates that may leave you unprotected in court.

Lead-Based Paint Disclosures: Required for properties built before 1978.

Eviction Notices: Follow local protocols for serving eviction forms if necessary.

Security Deposits: Keep tenant deposits in a separate trust account, as required by law, and document any deductions with receipts and photos.

3. Rent Collection: Streamlining Payments

Efficient rent collection ensures consistent cash flow. Here’s how to optimize the process:

Automate Payments: Use online systems that allow tenants to set up automatic payments or pay electronically.

Incentivize Timely Payments: Offer small perks for tenants who consistently pay on time, such as discounts or credits.

Enforce Late Fees: Clearly communicate and enforce late fees to encourage responsible payment habits.

4. Maintenance and Repairs: Addressing Issues Proactively

Prompt maintenance not only keeps tenants happy but also protects your property from long-term damage.

Online Maintenance Requests: Provide a simple way for tenants to report issues, such as through a mobile app or website.

Immediate Response to Emergencies: Have a plan in place for urgent issues like flooding or electrical problems.

Avoiding “Landlord Specials”: Cheap, rushed fixes can lead to higher expenses over time. Prioritize quality over shortcuts.

5. Tenant Satisfaction: Hospitality Mindset

Borrowing from the hospitality industry, treating tenants as valued customers can significantly improve retention.

Clear Communication: Keep tenants informed about maintenance schedules, policy updates, or lease renewals.

Flexibility with Rules: While staying consistent with policies, accommodate tenant needs when possible, such as adjusting rent due dates to align with their paydays.

Add-On Services: Offer extras like lawn care, renters’ insurance, or appliance rentals to enhance tenant convenience and generate additional income.

Self-Management vs. Professional Management

Self-Management

Managing properties yourself can save money, but it’s time-intensive and requires in-depth knowledge of legal and operational best practices.

Pros:

Emotional involvement, especially with difficult tenants.

Professional Property Management

Hiring a professional property manager can streamline operations and protect your investment, but it comes with a fee (typically 6–12% of rent).

Pros:

Expertise in tenant screening, legal compliance, and maintenance.

24/7 availability for emergencies.

Freedom to focus on scaling your portfolio.

Cons:

Additional costs reduce immediate cash flow.

Ultimately, if managing properties feels overwhelming or detracts from other priorities, outsourcing management to a qualified professional is often worth the expense.

How to Choose the Right Property Manager

When selecting a property management company, look for:

Experience: They should have a solid history of managing your specific property type (e.g., short-term rentals, multi-family units).

Technology: Ensure they provide online portals for both owners and tenants, with detailed monthly reports on income, expenses, and maintenance.

Transparent Fees: Ask about leasing fees, renewal fees, and how add-on income (e.g., pet fees) is handled.

Reputation: Seek referrals and read testimonials from current clients.

Communication: Evaluate how promptly they respond to inquiries and how they handle tenant interactions.

Key Takeaways

Tenant Screening is Critical: Thorough tenant screening minimizes risks and ensures reliable rent payments.

Stay Legally Compliant: Use professional leases and keep up with landlord-tenant laws to avoid costly mistakes.

Automate Rent Collection: Online systems reduce friction and ensure consistent cash flow.

Value Tenant Relationships: Treat tenants like valued guests to encourage long-term occupancy.

Prioritize Maintenance: Address issues quickly to avoid expensive repairs and maintain tenant satisfaction.

Consider Professional Management: Outsourcing can save time, protect assets, and improve cash flow in the long term.

Conclusion

Property management is a dynamic and multifaceted responsibility, but with the right strategies, tools, and mindset, it can be highly rewarding. Whether you choose to self-manage or hire professionals, focus on creating efficient systems, maintaining strong tenant relationships, and protecting your investments. By doing so, you can maximize both profitability and peace of mind.

Remember, successful property management is about consistency, education, and treating your rental properties not just as real estate but as thriving assets. The effort you invest today will pay dividends in the years to come.

Streamline tenant screening with our free checklist tool! Evaluate credit, background, and more to find the perfect renter easily.

Tenant Screening Made Simple for Landlords

Finding the right renter for your property can feel like a daunting task, but having a structured approach changes everything. A well-organized tenant evaluation process ensures you cover all the bases—credit history, past rentals, employment status, and more—without getting overwhelmed. Our tool is designed to help property owners navigate this journey with confidence, turning a complex chore into a straightforward checklist.

Why Thorough Screening Matters

Renting out your space is a big decision, and skipping key steps can lead to costly mistakes. By systematically reviewing a potential renter’s background, you minimize risks like missed payments or property damage. Think of it as due diligence; a little time upfront can protect your investment for the long haul. Beyond just checking boxes, understanding why each criterion matters—like verifying income stability—empowers you to make informed choices.

Keep Records, Stay Organized

One of the biggest perks of using a renter vetting checklist is the ability to track your progress. Documenting each step, from initial application to final decision, keeps everything in one place. Whether you’re managing one unit or several, staying organized with clear records helps you avoid mix-ups and ensures fairness in your process. Try our tool today and see how easy it can be!

FAQs

Why is a credit check so important when screening tenants?

A credit check gives you a window into a tenant’s financial responsibility. It shows if they’ve got a history of paying bills on time or if there are red flags like unpaid debts or bankruptcies. While it’s not the whole picture, it helps you gauge whether they’re likely to pay rent consistently. Just remember to get their written consent before running the check—it’s a legal must in most places!

How do I verify a tenant’s rental history effectively?

Start by asking for contact info of their previous landlords on the application. Then, reach out directly—don’t just rely on what the tenant tells you. Ask about their payment history, any damages, and if they followed lease rules. If a tenant hesitates to provide this info, that could be a sign they’ve got something to hide. It takes a little effort, but this step can save you headaches down the road.

What should I look for in personal references?

Personal references can reveal a tenant’s character, but you’ve gotta ask the right questions. Focus on how long they’ve known the tenant and if they’d trust them in a rental situation. Keep in mind, though, that most people pick references who’ll say nice things, so don’t weigh this too heavily. Pair it with hard data like credit or background checks for a fuller picture.